Nathaniel Prescott, Lead Wealth Strategist & Solo Columnist

June 30, 2026 · 16 min read

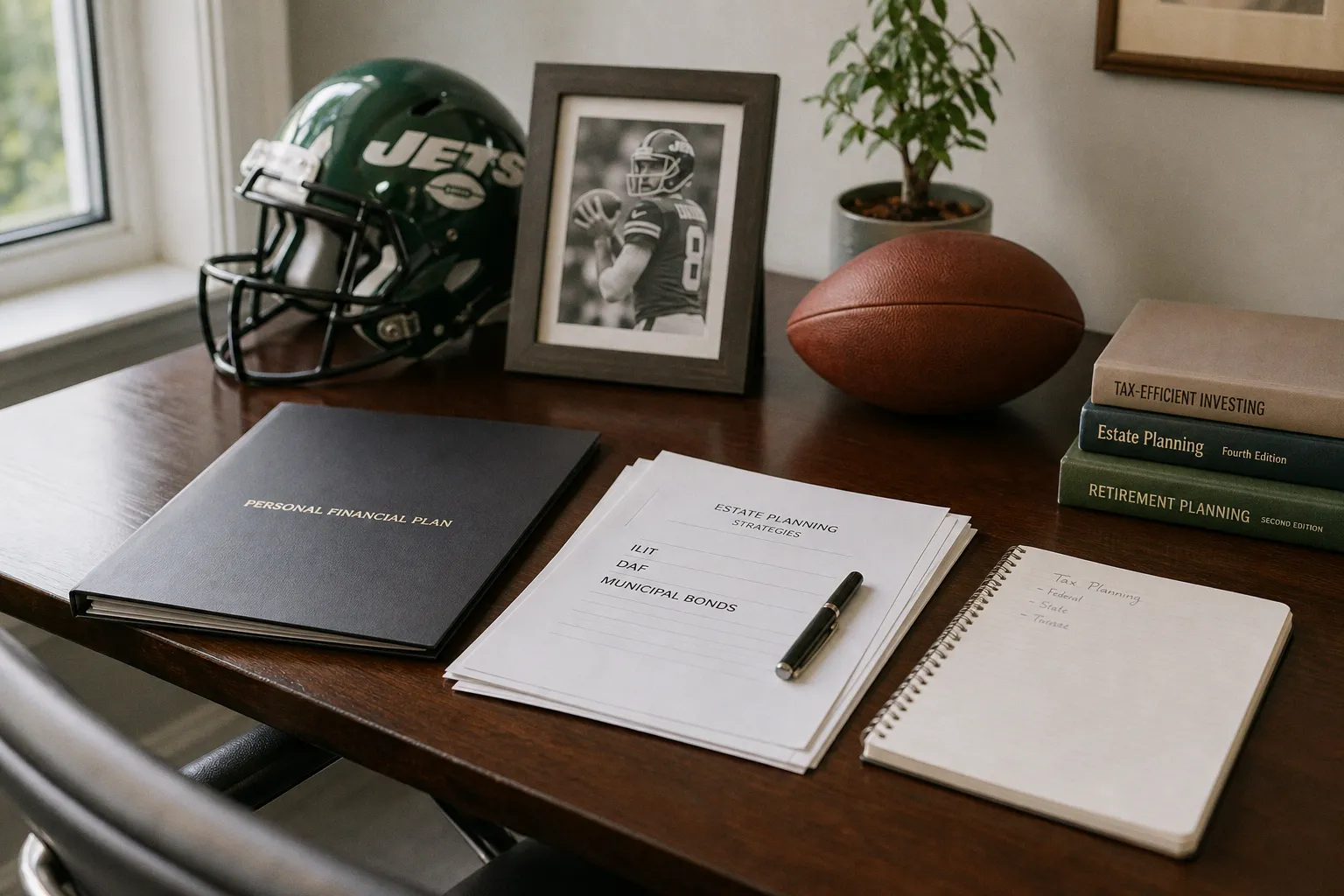

Avoid Aaron Rodgers Post Retirement Plans for Tax Savings

Aaron Rodgers has earned more than $300 million in NFL salary alone. That number creates a predictable internet reflex: assume there must be some brilliant, hidden tax maneuver behind his next move. A trust. A residency shift. A charitable structure.

Here is the problem: there is no credible public evidence of specific Aaron Rodgers post retirement plans for tax savings. None worth building a portfolio decision around. What we do have is a familiar mix of celebrity finance speculation, contract headlines, and generic high-net-worth tax strategies being stitched together into something that sounds more actionable than it is.

That is dangerous. Not because Rodgers is irrelevant. He is a useful case study precisely because he sits at the intersection of athlete income, multi-state taxation, endorsement economics, and post-career wealth preservation. But if you are using rumored celebrity tax planning as a model for your own retirement strategy, you are already starting from the wrong side of the spreadsheet.

The Myth of the Celebrity Tax Strategy

Celebrity finance content sells because it compresses complexity into a name. “What Aaron Rodgers is doing after retirement.” “How athletes avoid taxes.” “The wealth playbook of NFL stars.” Clean headline. Bad framework.

Tax planning for someone with nine figures of career income is not one strategy. It is a stack of constraints. Federal rates. State residency. endorsement income. investment income. estate planning. liquidity needs. family obligations. charitable intent. asset protection. post-career business ventures. Every piece creates drag somewhere else.

The highest federal marginal income tax rate is 37% for 2024 and 2025. On top of that, certain investment income can face the 3.8% Net Investment Income Tax. Then come state taxes, local taxes, and the athlete-specific mess known as the jock tax. None of this gets solved by copying a headline.

Rodgers did restructure his New York Jets contract in 2023. That is a confirmed public fact. The stated football purpose was salary cap flexibility. That does not tell us his estate plan. It does not reveal his trust architecture. It does not prove a tax minimization scheme. Contract restructuring can affect timing, cash flow, guarantees, and cap accounting. It is not automatically a personal tax blueprint.

A celebrity contract headline is not a retirement plan. It is a data point with missing columns.

We should be blunt about this: most public commentary around Aaron Rodgers post retirement plans is speculation dressed up as analysis. The market does this constantly with famous people. It takes standard tools used by wealthy households — donor-advised funds, municipal bonds, irrevocable trusts — and implies the celebrity is using them. Maybe he is. Maybe he is not. Without evidence, we do not build conclusions.

Investors should care because the same error shows up in normal retirement planning. People see what a wealthy person supposedly does and ask, “Should I do that?” Usually the better question is: “What problem was that structure designed to solve?”

A $2 million retiree, a $20 million business owner, and a $300 million athlete do not have the same tax problem. They may use some of the same tools. They should not use them in the same way.

The Jock Tax Is Not a Footnote

Professional athletes are taxed across multiple jurisdictions because they earn income in many places. This is commonly called the jock tax. It sounds like trivia until you see how it affects planning.

An NFL player can owe taxes in states where games are played, not only where he lives or where his team is based. The allocation rules vary. The filings multiply. The compliance burden is real. For a player with large salary income, bonuses, endorsements, and investment assets, tax season is not a folder of W-2s and a brokerage 1099. It is a jurisdictional audit map.

For retirement planning, this matters because the tax problem changes after active play ends. The athlete moves from earned income to investment income, deferred compensation, business income, endorsement residuals, and potential pension or league benefits. The state footprint may shrink. Or it may not, depending on business activity, residency, and income sourcing.

For ordinary investors, the lesson is not “move to Florida tomorrow.” That is lazy. The lesson is that tax location matters only when it is integrated with the full balance sheet.

A residency change can be rational. It can also be cosmetic. If you claim a low-tax state but keep meaningful ties elsewhere, you invite scrutiny. Tax agencies understand wealthy people. They know the difference between a real domicile change and a paper exercise.

Here is the practical version:

| Planning issue | Active NFL player | Retired high-net-worth investor | Normal retiree |

|---|---|---|---|

| Earned income footprint | Multi-state game allocation and team compensation | Usually lower, but may include business or media income | Often limited or absent |

| Investment income | Secondary during peak earning years, but growing fast | Central planning concern | Central planning concern |

| State tax exposure | Complex and recurring | Depends on domicile, asset location, and income sourcing | Depends heavily on residence and withdrawal strategy |

| Tax planning priority | Cash flow, withholding, entity structure, compliance | Estate design, capital gains control, charitable strategy, asset protection | Withdrawal sequencing, Roth strategy, Social Security taxation |

| Biggest risk | Confusing gross income with durable wealth | Over-structuring or fee-heavy products | Poor withdrawal timing and tax-bracket waste |

The athlete version is louder. The retiree version is quieter. The arithmetic is still the arithmetic.

If you are planning your own retirement, do not start with celebrity residency rumors. Start with your taxable income stack: pensions, Social Security, required minimum distributions, brokerage dividends, capital gains, Roth assets, rental income, business income. Then model the sequence. Taxes are not minimized in isolation. They are managed across time.

Standard Tools Are Not Secret Weapons

High-net-worth households often use several legitimate wealth preservation tools. These are not magical. They are not “loopholes” in the cartoon sense. They are legal structures with trade-offs.

The common toolkit includes irrevocable life insurance trusts, donor-advised funds, municipal bonds, family limited partnerships in some cases, grantor trusts, Roth conversion strategies, tax-loss harvesting, qualified opportunity funds, and direct indexing. Some are useful. Some are oversold. Some are terrible when used by the wrong person for the wrong reason.

Let’s separate function from marketing.

Irrevocable Life Insurance Trusts

An Irrevocable Life Insurance Trust, or ILIT, is typically used to keep life insurance proceeds outside of the taxable estate, assuming it is structured and administered properly. For very wealthy families, that can matter. Estate liquidity matters when heirs may face estate taxes, illiquid assets, or concentrated business interests.

But an ILIT is not free flexibility. Irrevocable means you give up control. Premium funding must be handled correctly. Crummey notices, trustee duties, gift tax reporting, and policy management are not decorative details. They are the operating system.

If your estate is not exposed to estate tax and your liquidity needs are simple, an ILIT may be complexity cosplay. Wall Street and insurance distributors love complexity because complexity justifies compensation.

Donor-Advised Funds

A donor-advised fund allows a taxpayer to make a charitable contribution, potentially receive a deduction in the contribution year, and recommend grants over time. For high-income years, that can be useful. A professional athlete with uneven income could, in theory, benefit from bunching charitable contributions during peak earning years.

But again, we do not know whether Rodgers uses one. We only know DAFs are common among high-net-worth individuals.

The investor lesson is cleaner: charitable strategy should be timed against tax brackets. If you expect one unusually high-income year — business sale, large bonus, equity compensation event — bunching deductions may be more efficient than spreading gifts evenly. If you are charitably inclined and over age thresholds for qualified charitable distributions later in retirement, the planning changes again.

Charity is not just a deduction. It is capital allocation with a values screen. That does not mean it should be sloppy. If you want a non-financial reminder that capital and attention can be directed toward constructive outcomes, even a simple browse through positive news and human-centered stories is a useful counterweight to the usual panic feed. Then come back to the math.

Municipal Bonds

Tax-exempt municipal bonds can reduce taxable income, especially for investors in high brackets. The trap is yield drag. A tax-exempt yield is not automatically superior. You compare taxable-equivalent yield, credit risk, duration risk, state tax treatment, and portfolio role.

A 3.5% tax-exempt yield may beat a 5% taxable bond for a high-bracket investor. Or it may not. Depends on the bracket and the risk. The lazy version says “rich people buy munis.” The disciplined version asks whether the after-tax, risk-adjusted return is competitive.

Direct Indexing and Tax-Loss Harvesting

Direct indexing allows investors to own individual securities that mimic an index while harvesting losses at the position level. This can create tax assets. Useful in taxable accounts. Less useful in retirement accounts. Very useful for investors with large realized gains elsewhere. Less useful for investors with simple portfolios and low taxable turnover.

The sales pitch often implies tax alpha is endless. It is not. Losses are finite. Market behavior matters. Wash sale rules matter. Tracking error matters. Fees matter. The strategy can work, but it is not a money printer.

The wealthy do not avoid taxes by finding one magic structure. They reduce tax leakage by aligning timing, entity, location, and asset type.

That line is not exciting. It is also the truth.

Contract Restructuring Is Not the Same as Wealth Planning

Rodgers’ 2023 contract restructuring with the Jets created a wave of commentary. Some of it was football analysis. Some of it drifted into financial mythology.

NFL contracts are their own ecosystem. Salary cap treatment, signing bonuses, guarantees, incentives, void years, cash timing, and team accounting all matter. A restructure may help a team create cap room. It may change the timing of compensation. It may reflect negotiation leverage. But public contract reporting rarely gives you enough information to infer personal tax planning.

For a high-income athlete, compensation timing can matter. If income is accelerated or deferred, the tax year changes. If the player changes residency, the state impact may change. If income is characterized differently, the treatment may differ. But we should not pretend we know the personal side unless it is public.

The broader point for investors: cash flow timing is underrated.

Most retirement tax mistakes are not exotic. They are timing errors. Retirees let pre-tax accounts compound untouched for too long, then required minimum distributions shove them into higher taxable income later. They claim Social Security without understanding provisional income. They sell appreciated assets in a high-income year instead of harvesting gains in a low-income window. They ignore Roth conversions during the gap years between retirement and RMDs.

That is where real money leaks.

A celebrity athlete may have a team of attorneys and accountants solving a nine-figure version of the timing problem. You may have a seven-figure version. The principle is the same: the tax code rewards sequencing.

A decent retirement tax plan asks:

1. What income is already locked in each year?

2. Which accounts are taxable, tax-deferred, and tax-free?

3. What bracket are we filling now versus later?

4. Are capital gains taxed at 0%, 15%, or 20% under the current income picture?

5. Will Medicare IRMAA surcharges change the real marginal rate?

6. Are charitable gifts better made with cash, appreciated securities, or qualified charitable distributions?

7. Are heirs likely to inherit pre-tax assets at a worse tax rate than the current owner?

8. Is the estate large enough for federal or state estate tax exposure?

No celebrity rumor answers those questions for you.

The Real Tax Stack After Peak Earnings

The useful part of the Aaron Rodgers discussion is not whether he has a secret plan. It is what happens after a peak earner leaves the main income engine behind.

Athletes are extreme examples of compressed earning windows. They may earn more in 15 years than many professionals earn in a lifetime. The planning challenge is converting volatile, high-tax earned income into durable, flexible capital.

That transition has five serious components.

1. Liquidity Without Idle Cash

High earners often accumulate cash because income is large and decisions are delayed. Cash feels safe. Too much cash becomes opportunity cost. It loses ground to inflation and creates drag on long-term compounding.

The right liquidity reserve for a retired athlete with business ventures is not the same as for a standard retiree. But the principle holds: cash should have a job. Near-term spending, tax reserves, capital calls, property expenses, private investment commitments. Anything beyond that needs justification.

2. Concentration Risk

Athletes and entrepreneurs both tend to accumulate concentrated exposure. Private businesses, brand ventures, real estate partnerships, endorsement equity, or a single advisor-driven product shelf. Concentration can create asymmetric upside. It can also destroy wealth quietly before anyone admits the underwriting was weak.

The post-retirement portfolio should not be a trophy case. It should be a risk engine with controls.

3. Tax-Efficient Withdrawal Sequencing

For normal retirees, withdrawal sequencing is where tax planning becomes tangible. Spend taxable assets first? Convert traditional IRA assets to Roth? Preserve brokerage assets for step-up in basis? There is no universal rule.

The correct sequence depends on age, bracket, estate size, expected longevity, charitable intent, and market conditions. A low-income year after retirement can be valuable. Waste it, and you may lose a cheap Roth conversion window forever.

4. Estate Architecture

High-net-worth planning eventually becomes estate planning. The question shifts from “How do I pay less tax this year?” to “How do I transfer control, assets, and responsibility without creating a legal junk drawer?”

Trusts can help. They can also become expensive monuments to overengineering. The estate plan must match the family system. Who controls assets? Who receives income? Who can sell? Who pays tax? What happens after death, divorce, addiction, litigation, or incapacity?

If the answer is “the trust handles it,” you do not have an answer yet. You have a label.

5. Governance

This is the part finance marketing hates because it cannot be wrapped into a product. Wealth needs governance. Decision rules. Reporting. Investment policy. Tax coordination. Estate review. Insurance review. Advisor accountability.

For someone with major wealth, a family office may or may not make sense. There is no public evidence that Rodgers has one, and we should not invent that. But the concept is relevant: when assets become complex enough, coordination has value. The danger is paying institutional-level fees for institutional-looking theater.

Good governance reduces avoidable errors. Bad governance adds meetings.

What Ordinary Investors Should Actually Borrow

You should not borrow celebrity opacity. You should borrow discipline.

If we strip the name out of Aaron Rodgers post retirement plans and focus only on the financial mechanics, the real lessons are practical and unglamorous.

First, separate income planning from investment selection. Most investors obsess over funds while ignoring tax sequence. That is backwards. Asset allocation matters, but after-tax outcomes matter more than pre-tax bragging rights.

Second, build a tax map before you retire. Not the year after. Before. The valuable window often opens between your last paycheck and the start of Social Security, pensions, or required distributions.

Third, stop treating tax minimization as the only objective. A lower tax bill can be a bad deal if it increases risk, reduces liquidity, locks up capital, or forces you into high-fee products. The goal is not to pay the least tax in one year. The goal is to maximize durable after-tax wealth over decades.

Fourth, make your charitable strategy explicit. If you give, give intelligently. Appreciated securities may beat cash. Bunching may beat annual small deductions. Later in life, qualified charitable distributions may beat itemized deductions. The tactic follows the tax profile.

Fifth, document the rules. Rebalancing thresholds. Roth conversion bands. Capital gain harvesting limits. Cash reserve targets. Estate review dates. If your plan only exists in your head, it is not a plan. It is a preference.

Here is the simple version I would put in front of a serious pre-retiree:

| Decision | Bad default | Better framework |

|---|---|---|

| Roth conversions | “Convert or don’t convert based on vibes.” | Fill low-tax brackets strategically before RMDs begin. |

| Brokerage gains | “Avoid selling because taxes are bad.” | Realize gains when the bracket is favorable or risk is too concentrated. |

| Municipal bonds | “Buy because they are tax-free.” | Compare taxable-equivalent yield after credit and duration risk. |

| Charitable giving | “Write checks in December.” | Use appreciated assets, bunching, DAFs, or QCDs when they fit. |

| Estate planning | “Set up a trust because wealthy people do.” | Define control, tax, creditor, and inheritance objectives first. |

| Advisor selection | “Hire the person with access.” | Hire for coordination, fiduciary discipline, and transparent fees. |

That is not flashy. It works better than rumor mining.

The Discipline Behind Wealth Preservation

The most expensive phrase in personal finance is “people like that must know something.” Sometimes they do. Often they are surrounded by people selling complexity at premium margins.

Athletes, founders, executives, and inheritors all face the same core problem once wealth is created: preservation is less forgiving than accumulation. During accumulation, high income can hide mistakes. During preservation, mistakes compound in reverse. Bad tax timing. Bad private deals. Bad liquidity. Bad estate documents. Bad insurance. Bad advisors.

The public does not know Aaron Rodgers’ personal post-retirement tax strategy. We know he has had extraordinary career earnings. We know his 2023 Jets contract was restructured. We know athletes face multi-state tax complexity. We know high-net-worth households commonly use tools like ILITs, DAFs, and municipal bonds. That is where the evidence stops.

The correct investor response is not to fill the gap with fantasy. It is to translate the known facts into a better planning question.

If you are approaching retirement, your version of the problem is probably not a jock tax across NFL cities. It is taxable income control. It is whether your IRA will become a tax bomb at 73 or 75 under the rules that apply to you. It is whether your brokerage account is quietly overconcentrated. It is whether your heirs inherit flexibility or paperwork. It is whether your advisor is optimizing your balance sheet or merely managing assets for a fee.

Celebrity planning rumors give you noise. A tax projection gives you leverage.

So avoid Aaron Rodgers post retirement plans as a tax savings model. Not because Rodgers is doing anything wrong. Because you do not know what he is doing. Neither do the people packaging speculation as strategy.

You have two choices. Copy shadows from someone else’s balance sheet, or build a plan from your own numbers.

Only one of those compounds.